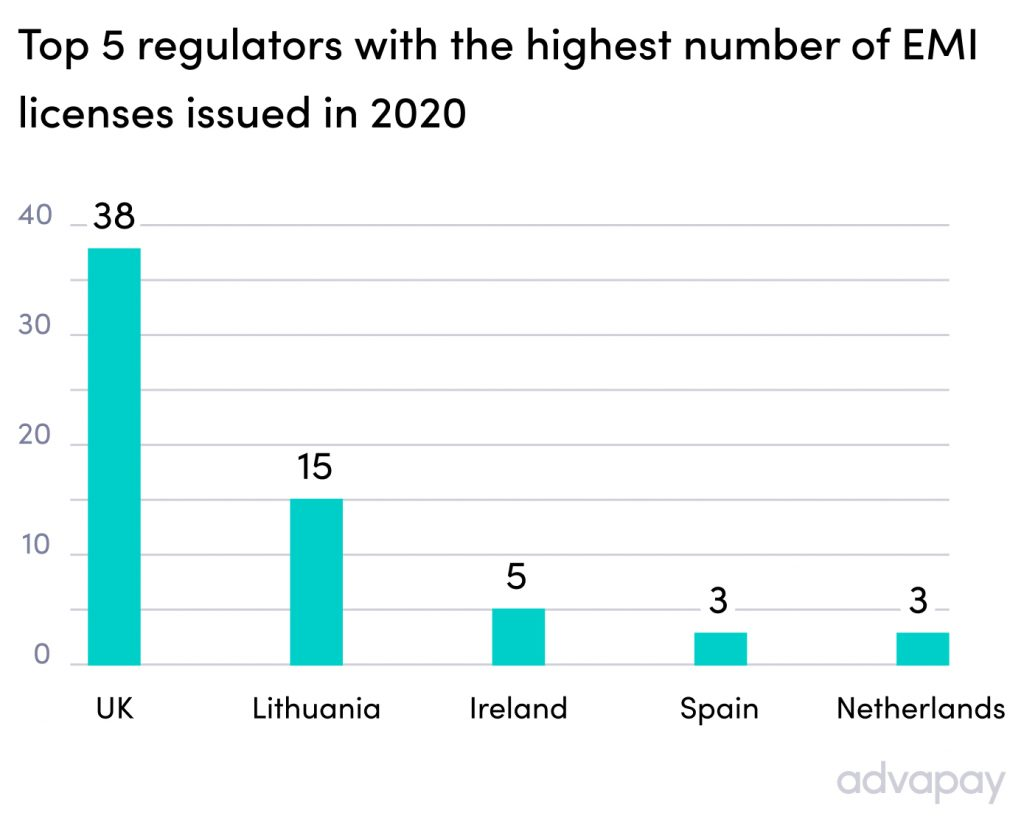

With challenger banks like Monzo, Revolut, Genome, and Monobank steadily growing in popularity, more and more financial bodies across the USA and Europe want to implement electronic money as one of their core offerings and become Electronic Money Institutions or EMIs. UK (Monzo) is the EMI licensing leader with 38 EMI licenses issued in 2020, while Lithuania (Revolut, Genome) follows suit with 15 licenses issued.

Due to the COVID-19 pandemic, this domain is on the rise, as using fiat money is proven to be one of the infection risk factors. Thus, people worldwide are more readily adopting online banking as their main source of payment, which means electronic money is a very lucrative and rapidly evolving domain.

Do you want to become an e-money institution yourself and reap the benefits of the existing situation? If so, read on to discover what is an electronic money institution, what EMI licensing types exist, how to obtain an EMI license, and what services an e-money institution can provide to its customers.

Let’s start!

E-money institution definition and key aspects

According to a definition from the European Central Bank, an e-money institution is a legal entity licensed to issue electronic money and perform operations with it. Electronic money is a monetary value deposited to digital or physical cards, which is accepted as the means of payment by merchants other than the issuer. To operate as an EMI, you need to obtain an electronic money license from some regulator, the UK-based FCA and the Bank of Lithuania being the most notable mentions in Europe.

There are two types of EMI licensing — to become an electronic money institution or an electronic payment institution (EPI). The core difference between them is that an EMI provides virtual banking accounts, where users can store money for any purpose, accrue interest on deposits, get loans, etc. WIth EPIs, every transaction should have a goal, so one can’t just deposit money to be used at a later date. This makes EMI services the best choice for digital banking, while EPI services are best used for currency exchange, e-Commerce checkouts and other immediate actions.

Here is a list of actions an electronic money institution can do:

- Open SWIFT, IBAN and SEPA accounts

- Remotely register banking accounts for companies and individuals

- Issue credit and debit cards for these accounts

- Perform wireless money transfers in more than 45 currencies

- Issue and accept payments via SWIFT

- Open correspondent accounts in various countries on behalf of your customers

- Get access to AML procedures to prevent fraud and money laundering

- Get VAT exempt in the country of your EMI license registration

While these capabilities allow building a very lucrative business, to start using them you need to undergo an EMI licensing process. Here is what you should do to obtain an EMI license.

How to obtain an EMI license

You must apply for an EMI license to the regulator of your choice. While some jurisdictions provide more stringent screening and some require less paperwork, the general set of documents and tools required to undergo EMI licensing is as follows:

- Company statutes

- Business plan

- Operations plan

- Proof of having the required minimum capital (above 300,000 GBP in the UK, i.e.)

- Description of having an anti-fraud tool in place to protect the invested funds

- Description of internal risk management, accounting, and administrative mechanisms

- Description of anti-money laundering and anti-fraud system configured

- Organizational structure overview

- List of key shareholder IDs and the proof of their ability to manage the company

- List of C-level management IDs and the proof of their good business reputation

- External auditor’s credentials

- Company registration address

As you can see, there are both technical and organizational requirements that should be met to ensure your EMI license application goes through successfully. Covery provides EMI license consulting and technical support to help you obtain the license.

What can an e-money institution do?

It is important to understand what actions are available to an EMI institution and what are your future growth prospects. Here is a non-exhaustive list of what you are allowed to do as an EMI:

- Operating payment accounts, depositing and withdrawing money from them

- Executing of payment transactions (credit transfers, direct debits, operations with payment cards)

- Executing of credit line transactions (credits, debits, payment cards)

- Acquiring payment transactions and issuing needed instruments

- Account information

- Payment initiation

- Remitting money

- Operating various payment systems

- Issuing and managing electronic money

One of the most important capabilities is transitioning from an EMI to a full-fledged online bank, which can be done through another straightforward application process.

Conclusions

Now you know what an electronic money institution is, how it differs from a payment institution, what it can do and how to apply for becoming one. Should you have any other questions or need assistance with EMI license consulting — contact Covery, we are always ready to help!