With the COVID-19 showing no signs of abating, 2021 can be a tough year for banks. Back in 2020, we saw a rapid growth of various fraudulent schemes (we covered the 5 most prominent fraud cases of 2020 in a separate article), but the trends in the banking industry worldwide have largely demonstrated the banks’ resilience, as well as the ability to adapt and innovate in the face of the crisis.

The pandemic forced the banking to do what the competition couldn’t have — evolve fast. The banks had to support the existing digital banking trends and provide mobile experiences instead of face-to-face communication with their customers in local branches — or go out of business.

New models of operations were introduced within weeks, hardware and software were updated using cloud computing technology. New policy measures were issued, aiming to sustain and prevail in the situation of lockdowns or even curfews. More than 3000 policy measures were registered at the World Bank in 2020, with more than 54% of them coming from the banking sector.

The challenges the banks faced and the approaches they took to overcome these challenges laid grounds for trends that will shape the business landscape in 2021. Read on to learn of the most important retail banking trends in 2021 and be able to prepare your business in advance, as forewarned means forearmed!

PWC highlights of 2020 in banking

PWC, the widely-known worldwide research conglomerate produced a detailed report on the way things stand in the retail banking domain in 2020. We provide several key insights from this report below:

- 61% of bankers affirm the importance of the customer-centric approach to doing business in 2021. Only 17% feel prepared to implement it.

- More than 57% of financial organizations struggle to acquire sufficient talent to achieve operational targets, especially in emerging markets.

- Industry-leading banks bolster their online presence and shift the emphasis from branch operations to digital dominance. Read the case of JP Morgan Chase launching the Dynamo neo-bank and creating 400,000 jobs in the UK without opening a single brick-and-mortar branch.

- Innovation is one of the key focal points for 2021, as 87% of survey respondents stated. Nonetheless, only slightly above 10% have sufficient expertise in place to support innovation.

- Proactive regulatory compliance management is also key, as 2021 will be the year the governments worldwide will start enforcing new regulations to structure the currently chaotic market. However, the majority of banks invested heavily in corresponding initiatives in the preceding years, and feel quite prepared for this situation.

As you can see, the key challenge the retail banks worldwide encounter lies in gaining access to sufficient expertise to ride the innovation wave and stay competitive. What’s more, 30% of customers stated their willingness to leave their primary banks for various fintech services due to unsatisfactory experiences during the pandemic, based on findings from Capgemini.

10 retail banking trends for 2021 by Capgemini

We provide a brief excerpt of an extensive report on retail bank technology trends for 2021 prepared by Capgemini and EFMA for the World Banking Report in 2020. The research is based on the following conditions of the existing business environment:

- A decade-long period of minimal interest rates.

- Operational turmoil due to the COVID-19 impact.

- High competition from fintech and challenger banks, especially for the Millennials and Gen Z, who form the new wave of customers.

- The necessity to work with diminished operational budgets and high capital lock-in.

- Upcoming changes and existing guidelines in the regulatory environment.

Thus said, below are the key 10 retail banking trends for 2021:

- The ongoing shift to digital banking requires integrated risk management approaches. Frankly speaking, the traditional banks that have no digital presence in 2021 will go out of business. Last year showed the customers they can do almost any interaction online, why should banking be an exception?

The neo-normal becomes the new backbone of banking. 2020 introduced lots of new financial and non-financial related risks (NFR), and the number of cyberattacks on banks grew by 238%. Thus. banks must be proactive to implement robust risk mitigation strategies and customer due diligence (CDD) mechanisms. - Simplifying operations to ensure cost optimization. The banks have to learn to do more with less and provide positive digital customer experiences with minimal expenses using advanced technologies. This means moving from on-prem virtualized environments to cloud-based Kubernetes clusters with Docker containers to minimize CAPEX and OPEX of running the IT operations. It also involves banking automation to reduce the number of repetitive actions the end-users have to do.

For example, the challenger banks like Revolut, Starling, or Monzo allow you to register a new bank account with 24, 38, and 45 clicks respectively — and the process takes a couple of minutes only. This is the power of KYC automation and built-in CDD checks for you, ladies and gents. With many traditional banks, it might take up to two days, not to mention you’ll need to do much more than 24 clicks in a banking app. - Introducing more cloud-based services and phasing out legacy infrastructure. With the majority of banks running their own data centers, the costs of maintaining IT operations are exorbitant. Prior to the pandemic, this was a price the banks agreed to pay — but now more and more stakeholders consider adopting a cloud-first IT operations approach to minimize the expenses on equipment maintenance and idle standby.

The catch here is that the regulation requires banks to store and process their customer’s sensitive data and PII in a secure environment. Despite the correctly configured cloud platform being the most secure digital environment that you can possibly imagine, banks are cautious about moving their troves of data away from their data center. There’s more to that — moving terabytes of data is not easy and quite costly.

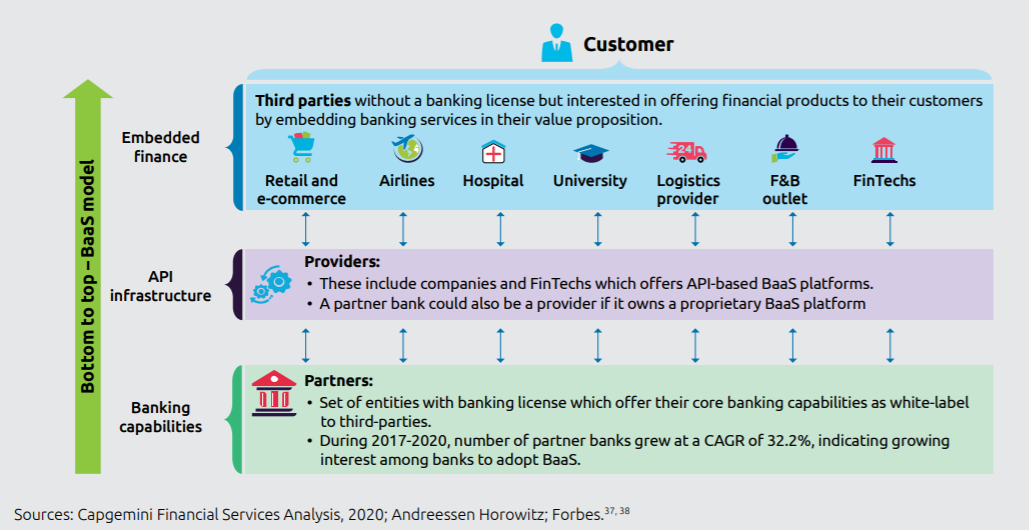

Thus, the prevalent approach is to build hybrid environments, combining the security controls of on-prem data centers with the scalability of the cloud. As a result, the customers receive blazing-fast banking app performance, while the bank enjoys the safety of mind and reduced IT infrastructure expenditure. - Banking-as-a-Service and Open Banking. There must not be war between banks and fintech companies. Instead, they can coexist and provide value to each other. For that, the banks should provide Open API access to their infrastructure so that fintech startups and other customers — retail, education, HoReCa, logistics, transportation, and others can build their offerings on top of it.

As a result, banks gain immediate access to a wide variety of tools they do not have to develop themselves (as well as new revenue streams in form of profit sharing, setup fees or subscriptions), while fintech and other partners acquire the computing resources they need — and access to the bank’s customer base to provide their products and services to. This helps the partner banks significantly reduce the customer acquisition costs — from $300-$500 to as low as $10-$20 per new user.

However, the potential for fraud is very high here, so due caution and strict security scrutiny must be exercised to avoid data breaches, both by external and internal actors.

- Green banking. With COVID-19 becoming the centerfold of all news pages for more than a year, it’s easy to forget about ecology and green initiatives. However, upholding and implementing them makes the banks more resilient to non-financial risk factors (NFRs). From lower carbon emissions to green credits for manufacturers — banks have lots of tools at their disposal to reinforce their brands and ensure customer base loyalty.

- Frictionless value delivery simplifies customer acquisition. With the traditional economy (manufacturing, heavy industry, construction, transportation) on hiatus, banks are looking for alternative ways to make revenue. Point-of-Sale financing for e-Commerce purchases hit the sweet spot back in 2020, with more than 60% of Millennials appreciating this opportunity. This way, they make a purchase online, get their money back at once and then pay them to the bank in chunks with some small interest instead of engaging in complex credit card schemes.

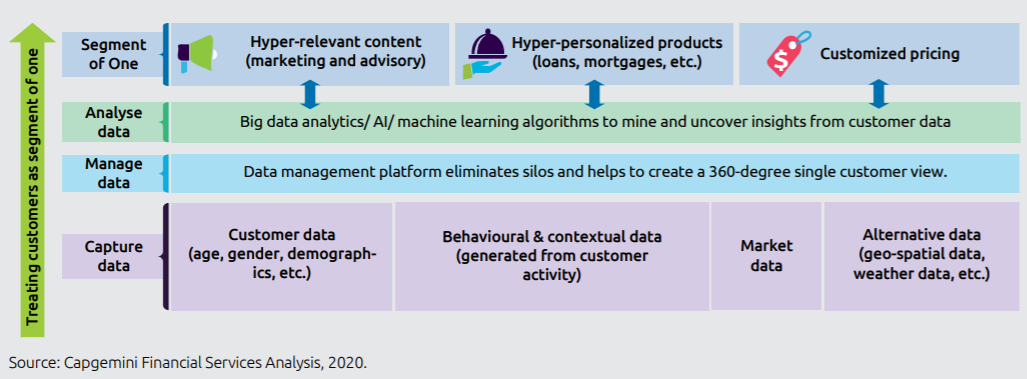

Other revenue streams include mortgage refinancing and wealth management, along with other activities. This way, banks help their customers find investment opportunities while the economy is not in full swing or help them save money on long-term expenses like mortgages. Such alternative lending schemes allow banks to make money — but they also expose the finances to risks of fraud from impostors. Thus said, checking the customer’s identity to prevent account takeover and synthetic identity theft is a necessary measure for every transaction. - Leveraging Big Data analytics to make hyper-personalized offerings. Banks already had troves of data on their customers. With more interactions online come new data sources, which result in improved efficiency and accuracy of analytics due to 360-degree customer view. This way, banks can employ a segment-of-one approach, treating every customer as a unique market segment, offering the services they need when they need it. This greatly increases customer satisfaction, brand loyalty and lifetime value, resulting in an improved bottom line in the end.

The point here is to be able to connect the dots and form holistic customer profiles out of disparate pieces of data. Device fingerprinting allows doing just that, helping track the customer’s purchase history and buying habits. As a result, banks improve the accuracy of upselling and cross-selling offers, as well as point-of-need suggestions acceptance rate.

- Re-bundling disparate services into one-stop shops. The key factor in favor of the first fintech platforms was the simplicity. They did not do a lot, but they did several things excellently — and people moved from complex bank accounts to an ecosystem of several tools. It’s normal to use one tool for cash flow monitoring, another for invoicing, yet another for payroll and benefits management. etc.

However, the story went full circle, and unbundling the services to simplify doing business resulted in the opposite — complex structure of interconnected tools. The next wave of fintech startups offers re-bundling the services through convenient aggregator platforms via APIs. Now, you can connect all of your toolkits and manage everything from a single convenient dashboard.

Banks can hop on the hype train and ride it, as they have all the infrastructure and tools in place to provide such aggregation — they just need to make the design better, UX seamless and management intuitive — which they can totally do. - The human touch in a digital world. While 73% of US bank customers interacted with their banks online prior to the pandemic, only around 20% stated they had an emotional connection to their bank. Without having human contact in the local branch office, the bank became just the tool, one that can be easily switched for another.

However, by possessing vast datasets on each customer and being able to use them to build hyper-personalized offers, retail banks are uniquely poised to add that human touch to their customer interactions. This will ensure a better customer experience, memorable user journeys, and deeper emotional connection with the bank, leading to the word of mouth promotion. And as you remember — when the tools are interchangeable, the customers easily switch to the one they LIKE more. - Reducing fraud through centralized transaction monitoring. According to Business Insider, there were an estimated $65 billion in losses due to fraud back in 2019, and the numbers are only going to grow. As the retail banking offerings grow in scope and variety, so do the fraud cases. Adding new services will open new attack surfaces and malicious intent vectors.

To cope with the challenge, banks implement monitoring and alerting measures well before releasing new products or services. However, running a bunch of monitoring systems for various niches is quite complex. This is why retail banking and fintech organizations consider moving to centralized risk management, fraud prevention and transaction monitoring systems.

This is quite a brief excerpt of an in-depth document providing a detailed overview of the current situation in the retail banking sector and the trends to follow in 2021.

Conclusions

As you might have noticed, Covery solves most of the challenges mentioned above. The hardships financial bodies face over the course of implementing the latest bank technology trends are already predicted and covered by our platform. We are glad our product vision and business evolution strategy are aligned with the insights of world-leading financial analytical entities.

Covery is an end-to-end fraud protection, chargeback prevention, KYC/AML verification, risk management, and transaction monitoring platform. It already provides all the features needed to support the emerging retail banking trends in 2021 — and it can do so much more!

Are you ready to find out how Covery can deliver value for your business? Contact us and let’s talk!